How Africa’s 2025 regulatory transformation is reshaping risk governance, financial integrity and operational resilience.

Introduction: A Turning Point for African Regulation

Africa is entering a period of regulatory transformation that is deeper and more structural than anything seen in recent decades. Unlike earlier cycles of reform that were often reactive or narrowly focused, the current evolution brings coherence and ambition, accompanied by a clear intent to align with global supervisory standards.

This shift is not only institutional; it represents a philosophical redefinition of what financial stability and good governance should look like in the continent. Regulators are moving away from regimes built on minimum compliance toward frameworks based on proactive oversight, macroprudential stability, financial integrity and digital resilience.

This new horizon places risk leaders at the center of Africa’s economic trajectory and challenges organisations to strengthen governance, modernise their systems and accelerate their capacity to respond to increasingly sophisticated regulatory expectations.

The Rise of Proactive and Standards-Aligned Supervision

One of the most defining elements of Africa’s new regulatory era is the embrace of proactive, forward-looking supervision. Authorities across the continent are accelerating their adoption of Basel III capital and liquidity rules, modernising their supervisory review processes and integrating climate, cyber and conduct considerations into prudential frameworks.

This change echoes a global transition toward continuous risk governance supported by real-time data, robust internal controls and strong organisational accountability. Markets such as South Africa, Kenya, Nigeria, Mauritius and Morocco are leading this shift, raising supervisory expectations for institutions operating under their jurisdiction. For risk teams, this trend requires more disciplined processes, more reliable data, and a stronger risk culture that can withstand sustained supervisory scrutiny.

Prudential Tightening: Liquidity, Capital and Governance Pressures

Africa’s financial sector is experiencing a more demanding prudential environment as a result of inflation persistence, elevated interest rates and currency volatility. The European Investment Bank’s report “Finance in Africa” highlights that these pressures are constraining liquidity and amplifying credit risk vulnerabilities across the region.

Regulators are responding by enforcing more stringent expectations around solvency, liquidity coverage and capital planning. Institutions must now demonstrate not only adherence to ratios such as LCR and NSFR but also the governance and analytical capabilities supporting those metrics.

Boards are expected to understand how stress scenarios affect their organisations, how liquidity buffers are maintained and how operational vulnerabilities interact with macroeconomic shocks. Prudential oversight has evolved from verifying compliance metrics to assessing whether institutions can truly withstand volatility.

Continental Integration: AfCFTA and PAPSS as Catalysts of Regulatory Convergence

Beyond national reforms, continental integration is reshaping Africa’s risk landscape in transformative ways. The African Continental Free Trade Area (AfCFTA), now ratified by more than 47 countries, is gradually pushing member states toward regulatory harmonisation in financial services, consumer protection, data governance and cross-border capital flows. This harmonisation reduces the risk of regulatory arbitrage and compels financial institutions to adopt more consistent and sophisticated compliance models across jurisdictions.

In parallel, the Pan-African Payment and Settlement System (PAPSS) is establishing a new backbone for intra-African payments by enabling direct, real-time settlement in local currencies. PAPSS eliminates inefficiencies associated with USD and EUR intermediaries, but it also introduces new forms of systemic risk, including liquidity synchronisation across borders, cyber vulnerabilities and operational dependencies on critical financial infrastructure. These continental developments require organisations to adopt a more regional and integrated perspective of their risk architecture.

AML/CFT Transformation: Beyond the Grey List

Africa’s journey in strengthening anti-money laundering and counter-terrorist financing frameworks has reached a decisive stage. With countries such as South Africa and Nigeria exiting the FATF grey list, the bar for AML/CFT compliance has been raised significantly. Supervisors are heightening expectations around beneficial ownership transparency, customer due diligence, monitoring of suspicious activities and regulation of virtual asset service providers.

Enforcement is becoming more visible, and cross-border cooperation is expanding. This evolution transforms AML/CFT from a narrow compliance function into a core component of financial integrity. Institutions that cannot demonstrate strong AML/CFT mechanisms now face heightened legal, financial and reputational risks, as global markets expect alignment with international standards.

Digitalisation, Cybersecurity and the New Rules of Operational Resilience

The rapid digitalisation of financial services across Africa has created a regulatory imperative to address operational and technological risks more rigorously. Mobile money, digital lenders, fintech platforms and cloud-based services have grown faster than supervisory frameworks could adjust—until now.

Regulators are catching up by issuing mandatory requirements focused on cybersecurity, operational resilience, incident reporting, technology governance and data protection. South Africa’s Joint Standard on Cybersecurity and Cyber Resilience is among the most comprehensive regulatory tools in the region and offers clear expectations around governance, incident management and digital continuity.

Elsewhere, central banks in Kenya, Nigeria and Ghana are implementing new directives governing outsourcing risk, cloud oversight, consumer protection and digital conduct. Cybersecurity is no longer an IT domain; it is now recognised as a systemic and prudential risk that requires integrated oversight.

Climate and Sustainability Regulation: From Peripheral to Mandatory

Africa is rapidly becoming an active participant in global sustainability regulation. Countries such as South Africa, Kenya, Nigeria and Egypt have introduced national green taxonomies aligned with international frameworks.

At the same time, multiple African jurisdictions have committed to adopting the ISSB IFRS S1 and S2 climate disclosure standards, which require organisations to integrate climate-related risks into governance, strategy, risk management and reporting.

This transition embeds climate and ESG risks into prudential supervision rather than treating them as voluntary or peripheral workstreams. For risk teams, this means developing the capacity to run climate scenario analysis, measure exposure to transition and physical risks, and build governance structures capable of overseeing sustainability performance.

The Risk Culture Gap: The Continent’s Most Underestimated Vulnerability

Despite regulatory progress, a significant operational challenge remains: many African organisations still manage risk through manual, fragmented processes heavily reliant on spreadsheets. This creates a widening gap between the level of regulatory ambition and the operational realities within institutions.

Weak risk culture, limited traceability, informal control environments and insufficient governance maturity frequently undermine compliance efforts. Supervisors increasingly expect a higher degree of integration across risk types, clearer lines of accountability, automation of critical processes and more reliable internal reporting.

Without meaningful improvements in risk culture and operational maturity, organisations will struggle to meet growing supervisory expectations.

Country Spotlights: South Africa and Ghana

South Africa stands as the region’s most advanced regulatory ecosystem. Its exit from the FATF grey list, mature prudential framework, strong data protection laws and ongoing development of the Conduct of Financial Institutions (COFI) Act make it a benchmark for regulatory sophistication.

In contrast, Ghana illustrates what regulatory transformation looks like under stress. The country’s post-restructuring environment, foreign exchange challenges, expansion of digital lending and climate reporting requirements have driven significant regulatory adjustments. Ghana’s experience highlights both the vulnerabilities and the adaptive potential present across African markets.

What African Risk Teams Must Do Now

Africa’s regulatory transformation demands structural changes in how organisations manage risk. To remain competitive and resilient, institutions must integrate and modernise their risk architecture, reduce fragmentation and reliance on manual tools, strengthen governance and board oversight, digitalise critical workflows, and embed cyber and climate considerations into their risk models.

They must also prepare for ongoing regulatory convergence across the continent, aligning internal frameworks with emerging regional standards driven by AfCFTA and PAPSS. Risk teams that invest early in these capabilities will not only meet supervisory expectations but will also position their organisations as leaders in a rapidly evolving financial environment.

Conclusion: Africa’s Emerging Regulatory Identity

Africa is not simply replicating global regulation; it is building a distinct regulatory identity shaped by international frameworks, regional ambitions and local realities. The continent is moving toward a more resilient, interoperable and strategically aligned financial system. For risk leaders, this represents both a challenge and an opportunity. Institutions that strengthen their governance, modernise their systems and embrace integrated risk management will play a central role in defining the financial future of the continent.

Are you ready to take the step and manage your risks with Pirani?

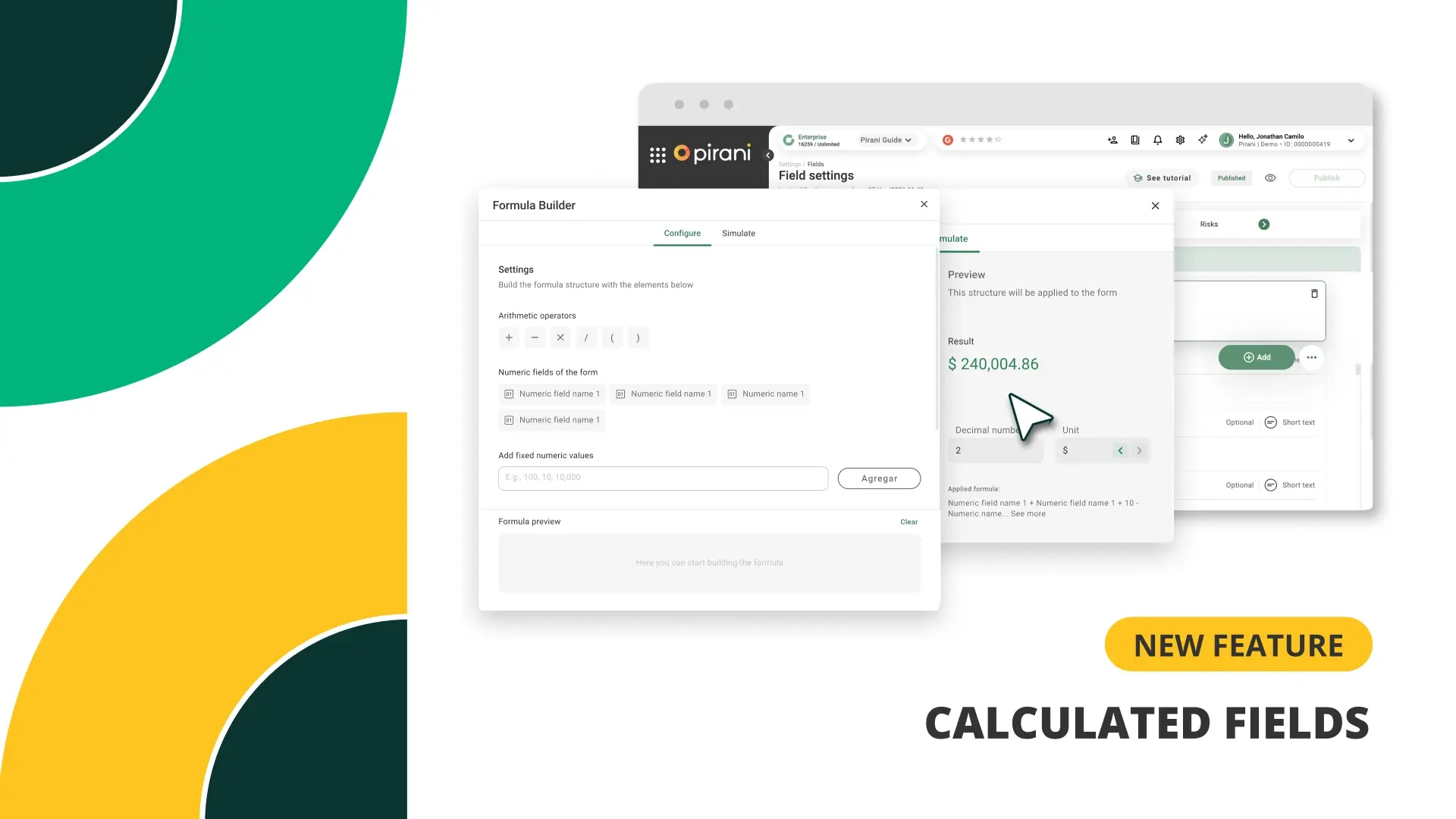

Calculated Fields in Pirani: Accurate, Automated Data

How to Identify When Your Risk Matrix Has Stopped Working