Preventing fraud in organizations is essential, particularly when it comes to money laundering and terrorist financing, two of the most serious threats businesses face today. The system used to combat these risks is known as Sarlaft (Risk Management System for Money Laundering and Terrorism Financing). This system is designed to help companies avoid becoming unwitting participants in illegal activities. Sarlaft serves as a tool for ensuring that companies’ financial activities remain transparent and free from the influence of illicit operations, thereby maintaining the organization's integrity.

While it may seem similar to financial risk management, Sarlaft has a distinct focus. It is built to proactively prevent, detect, and report risks related to money laundering and terrorist financing before they escalate. The system enables organizations to act quickly and effectively in response to potential threats, providing an essential line of defense against fraud.

Sarlaft is divided in two phases:

Using risk management software like Pirani, which includes modules specifically designed for fraud prevention, companies can easily identify, assess, control, and monitor risks associated with money laundering. These tools allow businesses to stay compliant with international regulations set forth by entities such as the Financial Action Task Force (FATF), ensuring their operations remain above board.

The Four Stages of Sarlaft

For Sarlaft to be implemented effectively, it must follow four key stages, which help ensure that fraud risks are adequately managed. These stages are:

- Identification: The first step is to recognize any risks that could potentially arise. This involves a thorough assessment of the company’s processes and transactions to identify areas where fraud might occur.

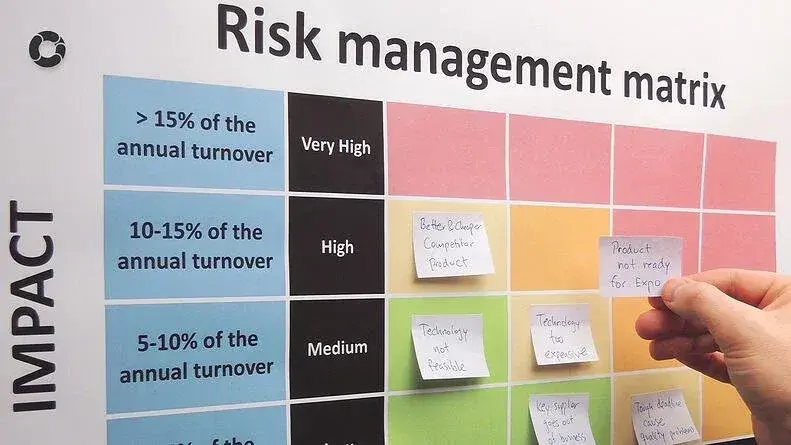

- Measurement: After identifying risks, the next step is to measure their likelihood of occurring and evaluate the potential impact they could have on the organization.

- Control: Once risks have been identified and assessed, companies must implement controls to manage them. This involves setting up procedures and strategies to prevent the risks from materializing or minimizing their impact if they do.

- Monitoring: Continuous monitoring is essential to ensure the control measures are effective. This step involves regular reviews of the system to detect any suspicious activities or changes in the risk environment.

Each of these stages plays a critical role in fraud prevention, helping companies remain vigilant and ready to address potential issues before they escalate.

Key Elements of Sarlaft

To ensure the successful implementation of Sarlaft, there are several essential elements that organizations need to consider. These components are crucial in supporting each stage of the process and ensuring the system’s effectiveness in fraud prevention.

-

Policies

Companies must establish clear policies that guide the implementation of Sarlaft. These policies act as a framework for preventing fraud, outlining the rules and procedures that everyone involved in the process must follow. -

Procedures

Alongside policies, companies must develop and implement specific procedures to ensure that each stage of the Sarlaft process is carried out correctly. These procedures serve as a roadmap for preventing fraud and managing risks. -

Documentation

Keeping detailed records of every step taken during the implementation of Sarlaft is vital. Proper documentation allows organizations to track their progress and identify any potential gaps in their fraud prevention efforts. -

Organizational Structure

The organizational structure should clearly define who is responsible for each aspect of Sarlaft. Typically, senior management and the board of directors play a crucial role in overseeing the system, ensuring it is properly integrated into the company’s overall operations.

-

Control Bodies

Designating individuals or teams responsible for overseeing and evaluating the effectiveness of Sarlaft is essential. This group, often comprising internal and external auditors, plays a crucial role in identifying any irregularities or weaknesses in the system. Regular audits help ensure the company remains compliant with legal requirements and can adapt to any emerging fraud risks. -

Technological Infrastructure

An effective fraud prevention system requires the support of advanced technological tools. These tools enable companies to manage and monitor risks in real time, providing a robust foundation for detecting and responding to potential threats. -

Information Dissemination

Companies must ensure that both internal and external stakeholders are informed about the status of their fraud prevention efforts. Regular reporting provides transparency and helps stakeholders understand the effectiveness of the Sarlaft system. -

Training

Continuous training is essential for ensuring that the team responsible for managing Sarlaft is well-equipped to handle any fraud risks that arise. By keeping employees informed and trained on the latest fraud prevention techniques, companies can improve their ability to detect and respond to threats.

While Sarlaft is an effective tool for fraud prevention, its implementation can also give rise to additional risks. These risks need to be managed carefully to ensure they do not undermine the effectiveness of the system. Some of the most common risks include:

- Reputational Risk: If a company is linked to money laundering or terrorist financing, it risks significant damage to its reputation. This could lead to loss of business, decreased revenues, and legal challenges. Reputational risk must be carefully managed to maintain public trust and market confidence.

- Legal Risk: Companies face legal risks if they fail to comply with regulations related to money laundering and terrorist financing. This could result in fines, penalties, or lawsuits. Ensuring compliance with all relevant laws is critical for avoiding these legal challenges.

- Operational Risk: Operational risks arise from failures or inadequacies in the company’s processes, people, or technology. In the context of Sarlaft, operational risks could stem from weaknesses in the system’s implementation, which could lead to fraudulent activities going undetected.

- Contagion Risk: Contagion risk occurs when an organization is negatively impacted by the actions of an affiliate or partner. For example, if a partner company is involved in fraudulent activities, this could reflect poorly on the organization, leading to reputational damage or legal repercussions.

The Role of Technology in Fraud Prevention

Technology plays a pivotal role in the success of any fraud prevention strategy. By leveraging advanced tools and software solutions, companies can streamline their fraud detection and risk management processes. These technologies allow for real-time monitoring, data analysis, and reporting, giving companies the insights they need to stay ahead of emerging threats.

Solutions like Pirani’s fraud prevention modules are designed to help organizations manage their risks more effectively. These platforms provide a comprehensive view of potential threats, enabling companies to take swift action when necessary. By integrating technology into their fraud prevention efforts, businesses can significantly reduce their risk exposure and ensure their operations remain compliant with international standards.

Fraud prevention is a critical aspect of risk management for any organization, particularly in today’s increasingly complex financial landscape. By implementing a robust system like Sarlaft, companies can protect themselves from the dangers of money laundering and terrorist financing, while also ensuring compliance with international regulations.The key to successful fraud prevention lies in following a structured approach, which includes identifying, measuring, controlling, and monitoring risks. By supporting these efforts with the right policies, procedures, and technological tools, companies can safeguard their operations and maintain the trust of their stakeholders.

Moreover, organizations must remain aware of the additional risks that may arise from implementing a fraud prevention system, such as reputational, legal, operational, and contagion risks. By taking a proactive approach and continuously refining their strategies, companies can mitigate these risks and ensure long-term success in their fraud prevention efforts.

Source: Superintendencia Financiera de Colombia.

Learn 5 strategies to manage risk

Know 8 processes to identify risks

Main types of risk that can affect a company

Heat map: a tool to optimize risk management

Trends and Future in Operational Risk Management

No Comments Yet

Let us know what you think